Where is the Rupee headed?

"People know the

price of everything, but the value of nothing" - Oscar Wilde

Since

2008 we have seen sharp correction in rupee against major currencies of the

world. The INR has moved from 39 to 67 levels against dollar in 8 years which

numerically speaking is a 71% correction in 8 years or an almost 7% annualized

correction. Majority of us believe that we still have an inflation differential

of close to 4% with developed countries and that will be reflected in currency

depreciation. Consensus on the street suggests that INR will continue to lose

3-4% every year to remain competitive.

In

my opinion it’s extremely important to crystal gaze the relative value of rupee

against major currencies. Economics suggests that prices are determined by

supply and demand. RBI has kept supply of rupee in check for the last four to

five years due to which we witnessed deficit liquidity in that period. This was

primarily done to control inflation.

Contrary

to India, majority of developed countries were following easy monetary policy.

They tried to keep real interest rate negative to push up asset prices,

especially real estate.

·

Rupee Supply – RBI

today has structurally brought down inflation by keeping rupee supply in check.

There was limited monetary expansion due to this tightening of liquidity. Going

forward liquidity will ease and RBI will ensure steady expansion in money

supply which will increase supply of rupee in the system.

·

Rupee Demand – In

the past few years we have opened up our economy and allowed FDI in few of the

largest sectors of the economy like railway & defense. Passage of GST

constitutional amendment bill will encourage more FDI & FII flow in the

country. The stability shown by INR in the past three years is helping foreign

investors gain confidence. Fall in commodity prices has significantly improved

the balance of payment situation. Also in a world of monetary expansion, INR

being short in supply will start gaining because of demand supply mismatch.

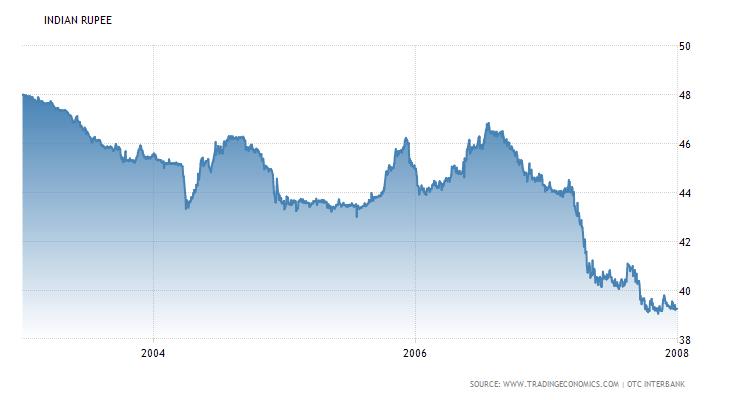

As

Carl Richard quotes – “Tomorrow’s Market Probably Won’t Look Anything Like

Today”. I would like to remind you all of a period between 2003 - 2008

where rupee gained against dollar over an five year period. Common sense tells

us that we are going to witness something similar.

We would like to put our thoughts on asset class behavior during time to come –

· Debt – Currency appreciation will create deflationary trend in the economy. In that environment rates will fall faster and deeper than what we anticipate. Majority of us are taking reinvestment risk in our portfolio by being on the shorter end of the curve. I would urge investors to lock their yield at a higher rate by investing in long term funds. Also I would urge people to buy quality and liquid papers where there is no credit risk.

· Equity - Currency appreciation will help majority of domestic facing companies primarily due to lower input cost. GST and FDI in railway & defense will also help towards this cause. I would urge investors to look at domestic facing companies from auto, auto ancillary, FMCG, engineering, cement, logistics and other allied manufacturing industry as they look poised to create a multiyear trend.